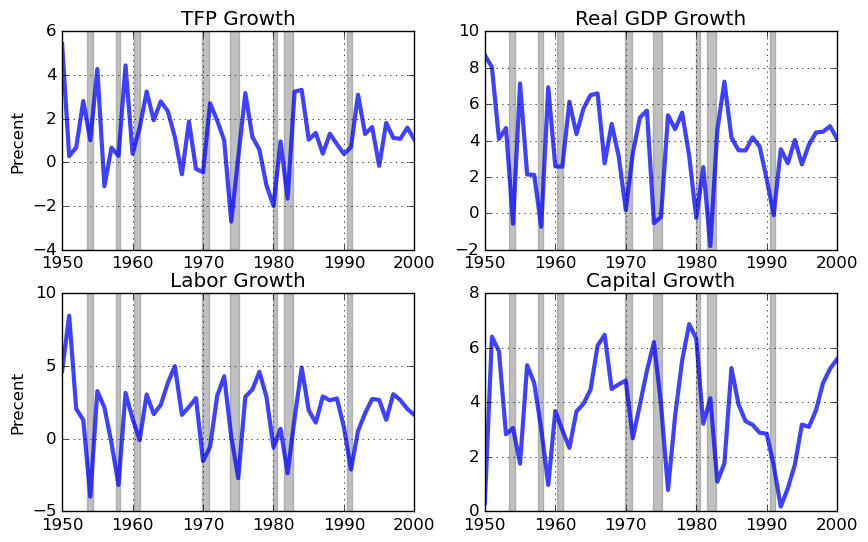

Production Data

The following are links to csv files containing selected data from the US National Income and Product and Product Accounts (NIPA) and a constructed measure of the US capital stock:

- Annual: levels and growth rates

- Quarterly: levels and growth rates

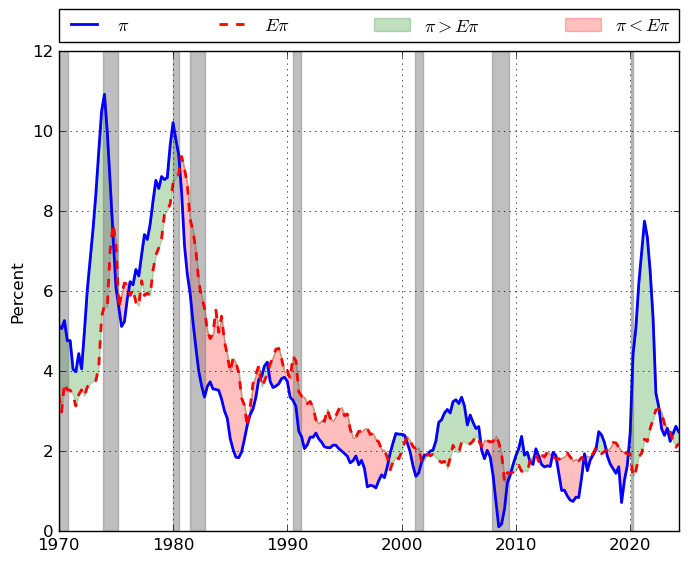

Source: Federal Reserve Economic Data - FRED.

Source: Federal Reserve Economic Data - FRED.